Stocks flirt with record highs as rate cut bets run wild

Stocks get another gift from Santa

Equities look set to end the year in buoyant form as the disinflation theme continues to fuel the rally in global risk assets. Shares on Wall Street extended their year-to-date gains on Tuesday after the final major data release of 2023 endorsed the view that central banks will begin to cut rates sooner rather than later.

Core PCE inflation in the United States slowed slightly more than expected in November, easing to 3.2% y/y from a downwardly revised 3.4% y/y in October. Personal consumption was subdued for a second month but without flashing any alarm bells, all of which support the soft landing narrative.

Expectations for Fed rate cuts strengthened on the back of the data and markets are currently pricing in around 155 basis points of cuts by December 2024, widening the gap with FOMC members’ own predicted rate path.

Is inflation dead?

In the absence of any new inflationary threat and clear evidence that the American economy is no longer running on all cylinders, there’s little reason for traders at the moment to be as cautious on the inflation outlook as policymakers are.

Everything points to a slowing economy and an inflation trend that’s firmly headed downwards, so a rate cut as early as March is not that inconceivable. If there is anything that can spoil this optimism, it is an upside surprise in the next jobs report. Weekly jobless claims have been somewhat lower in December compared to November, so a strong payrolls print is possible in next week’s report. But until then, there’s little that’s likely to get in the way of the risk rally.

Global stock rally gathers pace

The S&P 500 closed at a record high on Tuesday and came close to beating its all-time intraday high from January 2022. The Nasdaq 100, meanwhile, climbed further in uncharted territory, closing at a new record peak.

The upbeat mood is continuing today in Asia and Europe where many markets are reopening after the long Christmas weekend. Shares in Hong Kong and China are some of the best performers as gaming stocks have rebounded after Beijing stepped in to reassure investors about its plans for new regulatory curbs for the gaming industry following last week’s surprise announcement that triggered a sharp selloff.

Dollar mixed as yen struggles after BoJ Summary

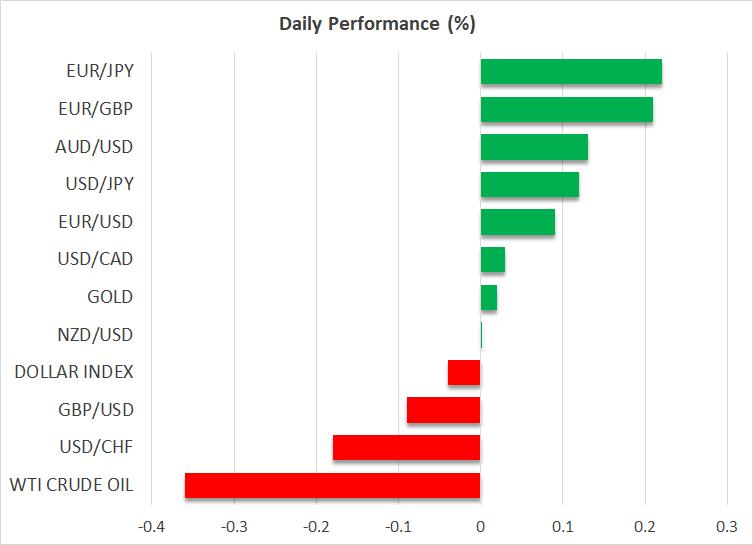

It was a slightly different picture in FX markets, however, as the major currencies were subdued in thin holiday trade. The US dollar slid to fresh five-month lows against a basket of currencies, as it remained pressured from falling Treasury yields. The euro advanced further above the $1.10 handle, but sterling was slightly softer.

The Japanese yen was also weaker on Wednesday after the Summary of Opinions of the Bank of Japan's December policy meeting did not suggest that a rate hike was imminent. Policymakers appeared split on the need to make an early exit from stimulus. Comments from Governor Ueda on Monday indicated that the Bank is still waiting to see signs of more sustainable wage growth before making any decision.

If it wasn’t for the rate cut wagers for the Fed, the yen would likely be facing a steeper selloff right now. Nevertheless, with the dollar on the backfoot and the BoJ in wait-and-see mode, the yen might manage to hold steady for a while.

Daily Global Market Update

Weak PMIs Failed to Dampen GBPUSD

Eurozone PMI Temporarily Helps the Euro but Is Unlikely to Change the Trend

EBC Markets Briefing | Loonie closer to key support on easing policy

Stocks under pressure amid US election jitters, dollar extends gains

Technical Analysis – GBPJPY at 3-Month High

Has Bitcoin Completed a Correction?