Stock selloff eases but dollar’s wounds deepen amid tariff turmoil

Markets gripped by US recession fears

The selloff in equity markets appears to be easing on Tuesday even as shares on Wall Street bled heavily on Monday. Growing concerns that the Trump administration’s aggressive tariff policy is harming US businesses has stoked recession fears, fuelling expectations that the Federal Reserve will soon begin to slash interest rates.

Yet, sliding bond yields and Fed fund futures now implying about a 30% probability of a fourth rate cut this year have not been able to offer much support to equity markets. Investors are having to significantly downgrade their rosy earnings outlooks from soon after Trump’s election victory when it was expected that the boost to the economy from tax cuts and deregulation would far outweigh the damage from higher tariffs.

However, the resilience of the mighty US economy is being put to the test as businesses are reducing expenditure due to the uncertainty generated by the daily tariff headlines, while consumers are lowering their spending amid the layoffs in government departments.

No ‘Trump put’ for Wall Street

But at this point, it is President Trump’s constant flip-flopping on tariffs that is, more than anything, upsetting markets. Moreover, Trump seems willing to let the US economy endure some short-term pain to achieve his objectives on trade, and this is quite a turnaround from his first term when his administration was more sensitive to Wall Street’s reaction.

US stocks have lost more than $4 trillion over the past three weeks, with the Nasdaq 100 now officially in correction territory, having shed about 12% from its February record high, and the S&P 500 not far behind with losses of about 8.5%.

But there are some signs that the panic is subsiding as e-mini futures for the three main indices are positive today. High valuations likely exacerbated the selloff and there is possibly some dip buying, while some traders are potentially adjusting their positions ahead of tomorrow’s CPI report out of the US.

Gold eyes Ukraine talks

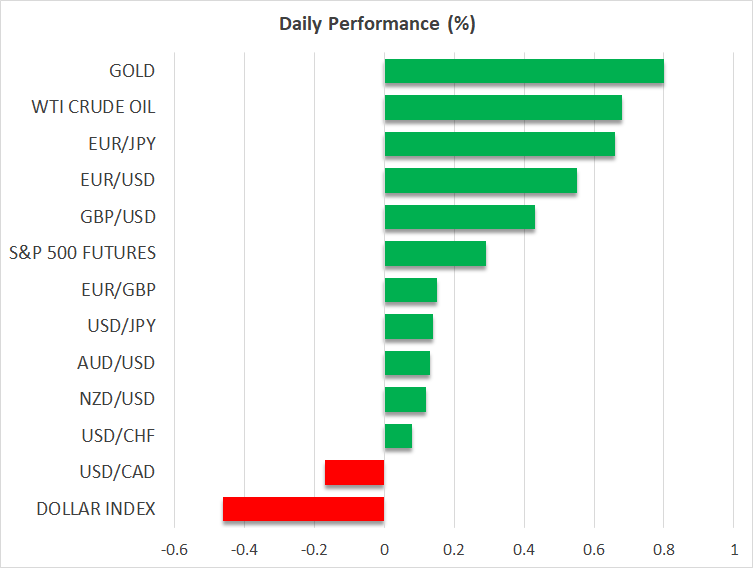

Gold has been somewhat muted during this tariff fallout episode, although it has climbed back above the $2,900 level today as investors await the outcome of high-stake talks due to take place between Ukrainian President Zelensky and US Secretary of State Marco Rubio in Jeddah, Saudi Arabia, today. Ahead of those negotiations, Ukraine appears to have carried out a drone attack on Moscow, which is thought to be the largest since the war began.

Other safe havens such as the Japanese yen and Swiss franc are off their latest highs, however, as the mood improves slightly.

Dollar’s woes not over as euro soars

The US dollar has bounced back above 147.00 yen after hitting a fresh five-month low of 146.52 earlier in the session. But against the euro and pound, the greenback continues to struggle.

Higher German bund yields are turbocharging the euro, which is testing the $1.09 level today. It comes as Germany’s Green party has signalled its willingness to negotiate with the CDU/CSU and SPD, who are likely to form the next coalition government, on their defence and infrastructure spending plans. The new government will need the support of the Greens to push through the reform of the debt brake rule needed to relax spending, as this requires two thirds of the votes in parliament.

Elsewhere, the Australian and New Zealand dollars were only modestly higher against their US counterpart. Despite China’s latest pledge of more stimulus to boost domestic consumption, the aussie and kiwi remain dogged by concerns about the impact of US tariffs on Chinese and global growth. The Canadian dollar, meanwhile, looked steady ahead of tomorrow’s policy decision by the Bank of Canada.

Markets experience subdued activity due to the Good Friday holiday: April 18, 2025

EBC Markets Briefing | Oil poised to rise with potential trade deals

EUR/USD in Equilibrium: Quiet Trading Expected on Good Friday

Markets Rattle as Trump’s 2025 Tariff Shock Triggers Global Sell-Off

USDJPY Analysis: appreciation trend of the yen has slowed down

Gold: epic rally

Can the AI chip boom survive a new tech cold war?