US CPI report could reverse the post-election euphoria

Mask joins Trump’s team, Germany sets election date

President-elect Trump is gradually assembling his cabinet, with the market anticipating the most crucial appointment, the Treasury Secretary. The latest addition to Trump's team was expected, as Elon Mask will lead the Department of Government Efficiency, with punters already accepting bets on how long the Trump-Mask relationship will remain rosy.

With Trump preparing for his new four-year term, the market is speculating about the timing of the tariffs’ announcements on imports, mostly from China. Europe is also expected to be targeted, with the European Commission frantically preparing for lengthy negotiations with the US and even tit-for-tat reactions.

These preparations will take place without the leadership of the euro area’s largest economy. Germany will hold a snap election on February 23, assuming that Chancellor Scholz loses the December 16 confidence vote. The continued weak economic performance, the budget hole and the active conflict in Ukraine will most likely dominate the pre-election campaign.

Interestingly, the latest polls show that no single party is likely to achieve an absolute majority. This means that lengthy negotiations to form another coalition government could delay even further the election of the new Chancellor, with the country potentially losing valuable time to counter Trump’s expected trade policy.

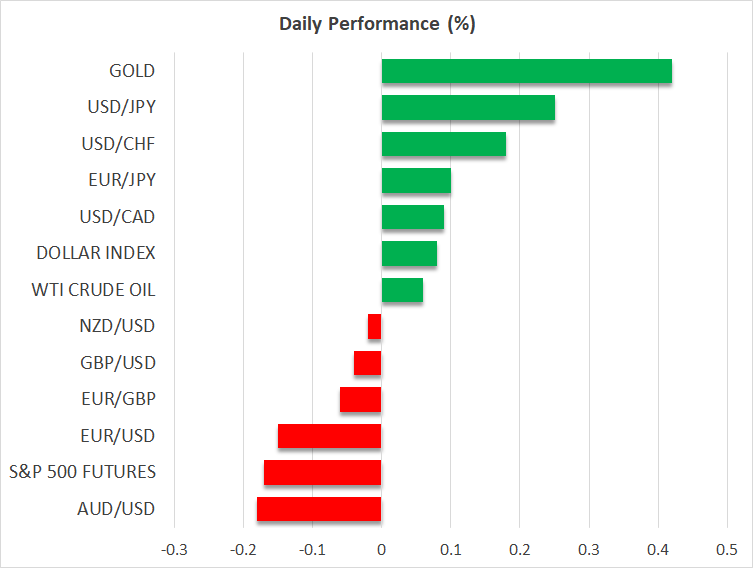

The post-US election rally takes a breather

Meanwhile, gold and bitcoin continue their journey in opposite directions. Gold is hovering around the $2,600 level, as the market is feeling more relaxed following the swift outcome of the US presidential election. At the same time, bitcoin recorded a new all-time high, almost touching the $90,000 level, with profit taking pushing it lower. It remains the biggest beneficiary of Trump’s win.

US CPI report in the spotlight

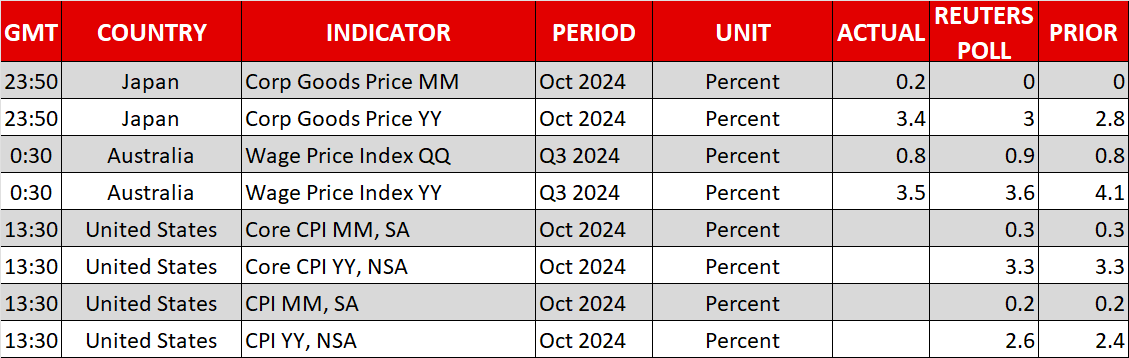

Similarly, US equities have partly retraced their steps, giving back a small chunk of their recent strong gains, due to profit-taking, with market participants potentially preparing for today’s important US CPI report. At 13:30 GMT, the October headline inflation rate is expected to show a 2.6% yoy increase, with the core indicator forecast to remain stable at 3.3%.

Economists are split about the possibility of an inflation surprise today. Proponents of an upside surprise point to the recent upward trend in the producer price index and last month’s hurricanes to justify their above-consensus call, while expectations for a downside surprise are based on lower demand due to the presidential election and the significant drop in oil prices during October.

An upside surprise could dent chances of a December Fed rate cut, thus boosting the dollar, particularly against the euro and the yen. On the flip side, a weak inflation report could go a long way into cementing a December Fed rate move. Fed members Logan, Musalem and Schmid are scheduled to speak today, and they could possibly express their view on today’s CPI report.

Yen’s weakness opens the door to intervention

Despite Japan’s stronger PPI report for October, the yen is again on the back foot against the dollar. This pair is testing the ¥155 level for the first time since mid-July, creating concerns among BoJ officials. While the yen’s ongoing weakness is expected to push inflation higher, BoJ officials are more focused on the wages front to justify further rate hikes.

Daily Global Market Update

Initial Jobless Claims Fuels Dollar

Gold Falls for the Fifth Consecutive Trading Session

EBC Markets Briefing | Oil prices ease as EIA raised output forecast

Dollar wavers on US CPI, surges on hawkish Fed remarks

Trump trade continues, US dollar rises on Wednesday Gold may fall towards $2500

AUDUSD remains in the red; sellers seem cautious