US stocks continue to vote down Trump’s tariff strategy

Trump’s U-turns keep the market under pressure

Both US equity indices and the US dollar remain under severe stress as US President Trump continues his back-and-forth on the tariffs front. In another U-turn yesterday, Trump decided to exempt products covered by the 2018 United States-Mexico-Canada Agreement (USMCA) from the recent imposition of 25% tariffs until April 2. This means that the majority of imports from America’s neighbours are again tariff-free for almost one month, until the reciprocal tariffs, which are expected to mostly target both China and the European Union, are announced.

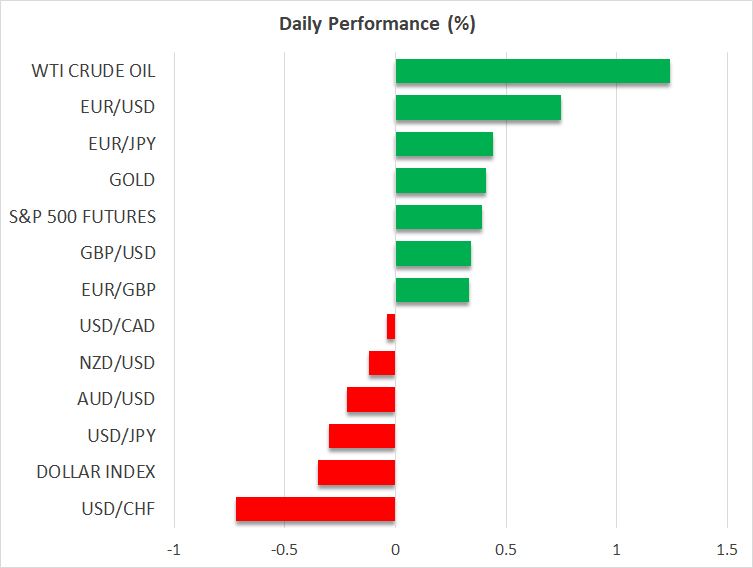

At face value, trade restrictions have a negative impact on both risk appetite and economic momentum. However, Trump’s current tactic of announcing tariffs and reversing his own decisions a few days later is even worse for sentiment, as it shows a lack of coherent strategy. Markets remain extremely confused, with US equity indices on course for their worst weekly performance since the first week of September 2024, when the Fed was preparing for the first rate cut of the current easing cycle. The Nasdaq 100 index is leading the selloff, with the Russell 2000 index also recording sizeable losses.

Fed is focused on nonfarm payrolls today

With the market remaining attentive to tariff headlines, the focus today shifts to the US data calendar and specifically the February jobs report. Following a decent 143k increase in January, economists forecast a 160k rise in nonfarm payrolls today, with estimates ranging from +30K to +300K, and a sizeable 142k jump in private payrolls. Both average earnings growth and the unemployment rate are expected to remain unchanged at 4.1% yoy and 4% respectively. Employment-related data this week, such as the employment subindices of the monthly ISM surveys and the weekly jobless claims, have been mostly positive, slightly opening the door to an upside surprise.

Today’s set of US data could offer a significant piece of the jigsaw to the Fed and help Chairman Powell et al. plot their strategy amidst Trump’s tariff strategy. A potentially weak labour market report today, coupled with softer inflation figures next week, could go a long way towards unlocking a rate cut in the next two Fed meetings. The market is currently pricing in 75bps of easing by year-end, with the first 25bps move expected at the June 18 gathering. Interestingly, Chairman Powell and Fed members Williams, Bowman and Kugler will be on the wires after the data releases.

ECB appears ready for a pause

The ECB announced another 25bps rate cut yesterday, but the overall rhetoric points to a pause at the April meeting following a series of consecutive rate cuts. This is not surprising, as the ECB is getting closer to the estimated neutral rate level, and eurozone countries, under the pretext of defense expenditure, are preparing for a significant increase in fiscal spending.

The euro continues to benefit from the apparent change in the eurozone's fiscal stance, with euro/dollar climbing to 1.0830 and recording its strongest weekly rise since mid-March 2009, when stock markets bottomed during the Great Financial Crisis. Similarly, the DAX 40 index is flirting with its best weekly performance since early December 2024. Notably, the DAX’s weekly outperformance over the S&P 500 index is 7.5%, which is the largest performance spread between the equity indices since March 2020, when the COVID pandemic was unfolding, and it is a strong indication that market participants are treating European stocks more favourably at this juncture.

Oil edges higher; cryptos disappointed from ‘Reserve’ announcement

Oil prices are climbing today, retesting the key $66.95-67.80 area, as participants try to find a new market balance. The selloff from the January 15, 2025 high has been significant and mostly confirms concerns about the global growth outlook. A strong set of US data later today could offer some respite to oil bulls, but tariff headlines remain a major headwind for the oil market.

Similarly, Trump’s Strategic Bitcoin Reserve failed to spur another rally in the crypto market as, contrary to expectations of a buying spree of major cryptocurrencies, the newly established Reserve will be funded by Bitcoin already owned by the US government. Bitcoin is hovering below the key $90k level today, with major alternatives suffering double-digit losses this week.

EUR/USD in Equilibrium: Quiet Trading Expected on Good Friday

Markets Rattle as Trump’s 2025 Tariff Shock Triggers Global Sell-Off

USDJPY Analysis: appreciation trend of the yen has slowed down

Gold: epic rally

Can the AI chip boom survive a new tech cold war?

Indices: investors switched to buying on downturns despite extreme fear

Dollar at the bottom: Tariffs ruin ‘exorbitant privilege’