Euro extends losses on French election jitters

Euro rocked by fresh fears of a debt crisis

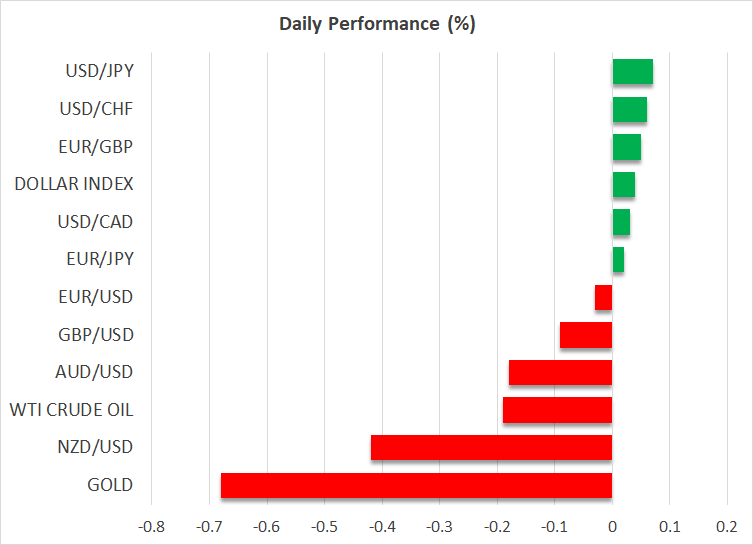

Concerns about the real risk of a far-right government in France continue to dog the euro after they resurfaced towards the end of last week. Having shed more than 1% so far in June, the euro is struggling to hold on to the $1.07 level on Monday and is currently trading at more than six-week lows.

Fears that a win for Marine Le Pen’s National Rally party in the snap legislative election at the end of the month would spark a market panic similar to the UK’s mini-budget episode under Liz Truss have driven the spread between French and German 10-year government bond yields to the highest since the summer of 2012 when the euro area was in the midst of the debt crisis.

But potentially a worse-case scenario for France than a Le Pen government is a hung parliament. After all, Italy’s Meloni has shown that far right parties are capable of becoming more mainstream. In France, however, the National Rally party has so far failed to form an alliance with a smaller far-right party and may therefore fail to gain enough seats to form a government, while President Macron’s coalition has also been unable to strike any deals, particularly as the centre-right Republicans, who are the most natural partners, are in disarray.

In a further blow for French assets, ECB sources have suggested that the central bank has no plans as of yet to buy French bonds in an emergency move to ease the panic in bond markets.

Stocks bounce back despite gloom

Nevertheless, France’s leading stock index, the CAC 40, is up today, recouping some of its losses.

Other regional indices also edged up on Monday as US futures turned positive, pointing to a slight easing in the risk-off mood. Wall Street’s rally lost steam on Friday as European election jitters and an unexpected drop in the University of Michigan’s consumer sentiment gauge triggered some profit taking. Though, for the week, the Nasdaq still managed to surge by more than 3% as the likes of Apple, Nvidia and Adobe powered ahead.

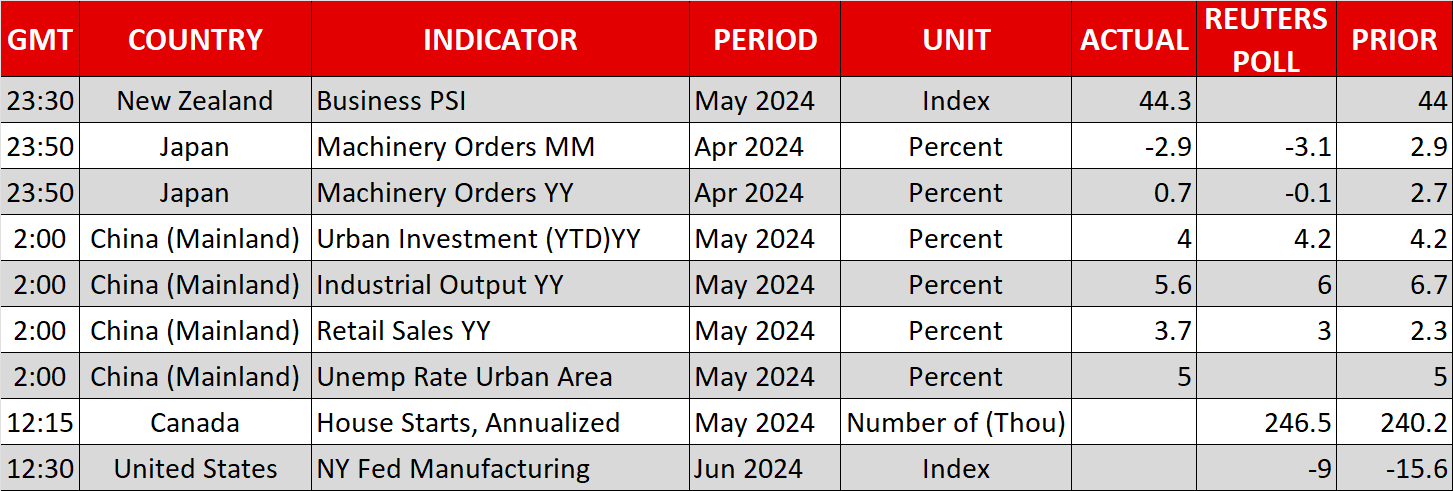

In Asia, however, stocks finished in the red after some mixed data out of China underscored the view that the economic recovery is stuck in the slow lane.

Aussie and pound on the backfoot ahead of rate decisions

The Australian dollar slipped on the Chinese figures and is on track for a third straight session of declines against its US counterpart. But there might be some support for the aussie from the Reserve Bank of Australia when it announces its latest policy decision tomorrow. The RBA will likely strike a hawkish tone as it keeps rates on hold, in contrast to the Swiss National Bank where investors have assigned a more than 70% probability of a 25-bps rate cut on Thursday.

The Bank of England also meets on Thursday, but the announcement looks set to be a low-key one amid the general election campaign in the UK and investors will be more focused on Wednesday’s CPI data.

The pound is battling election angst of its own amid growing fears that Labour would not stick to its pledge of keeping spending under control once in power.

As for the US dollar, Tuesday’s retail sales numbers will be the highlight along with Fed speakers, with Williams, Harker and Cook on the wires today.

Daily Global Market Update

All Eye on Today’s PCE

Dollar rebounds, loonie tumbles on Trump tariff threats

Crypto market deepens correction

EBC Markets Briefing | Bullion unchanged after Trump tariff vow

NZD/USD Hits Yearly Low Amid US Dollar Strength

Daily Global Market Update