Tariff turmoil sends dollar and Wall Street spinning

Tariff shock reverberates across markets

Global markets continued their meltdown on Thursday as Wall Street digested President Trump’s tariff blitz from a day earlier. It’s safe to say that there were no ‘Liberation Day’ celebrations for investors as the new tariff levels were far worse than what most were anticipating, fuelling fears of a global recession.

At the very least, a sharp economic slowdown seems certain in the US, not to mention a prolonged period of uncertainty, as even if Trump were to negotiate trade deals over the coming months that reduce some of the announced levy rates, higher tariffs are here to stay.

The long-term impact of Trump’s protectionist policies could take years to unfold, disrupting global supply chains and trade flows. This is heightening the jitters ahead of the Q1 earnings season, which kicks off next week and could flag the first cracks appearing in the US economy.

In the meantime, shares on Wall Street had their worst session since the 2020 Covid days on Thursday. The S&P 500 tumbled 4.8% to its lowest since August 2024, while the Nasdaq 100 nosedived by 5.4%.

Trump open to “phenomenal” offers

The selloff appears to be easing today, however, probably on the signs that Trump is open to lowering some of the tariffs. Speaking to reporters on Thursday, the President signalled that he would rethink some of the punitive measures if other countries offered something that was “phenomenal”, arguing that tariffs give the US “great power to negotiate”.

However, those comments have provided only a small boost, as Trump strongly indicated that sectoral tariffs on pharmaceuticals will be announced soon, likely followed by chip levies.

Whatever happens to the reciprocal tariffs, it seems that the specific duties on certain sectors are not negotiable. Aside from the fact that the Trump administration needs to raise billions to finance the promised tax cuts, ditching the sectoral tariffs would be a compromise too far given how strongly Trump feels about his “make America great again” mantra. But of course, he could yet change his mind if Wall Street continues to sink.

NFP report and Powell eyed

A ‘Fed put’ doesn’t seem likely either in the near future. Fed Chair Jerome Powell is due to speak at 15:25 GMT today and will probably maintain his wait-and-see stance even as the US economy is at a growing risk of stagflation.

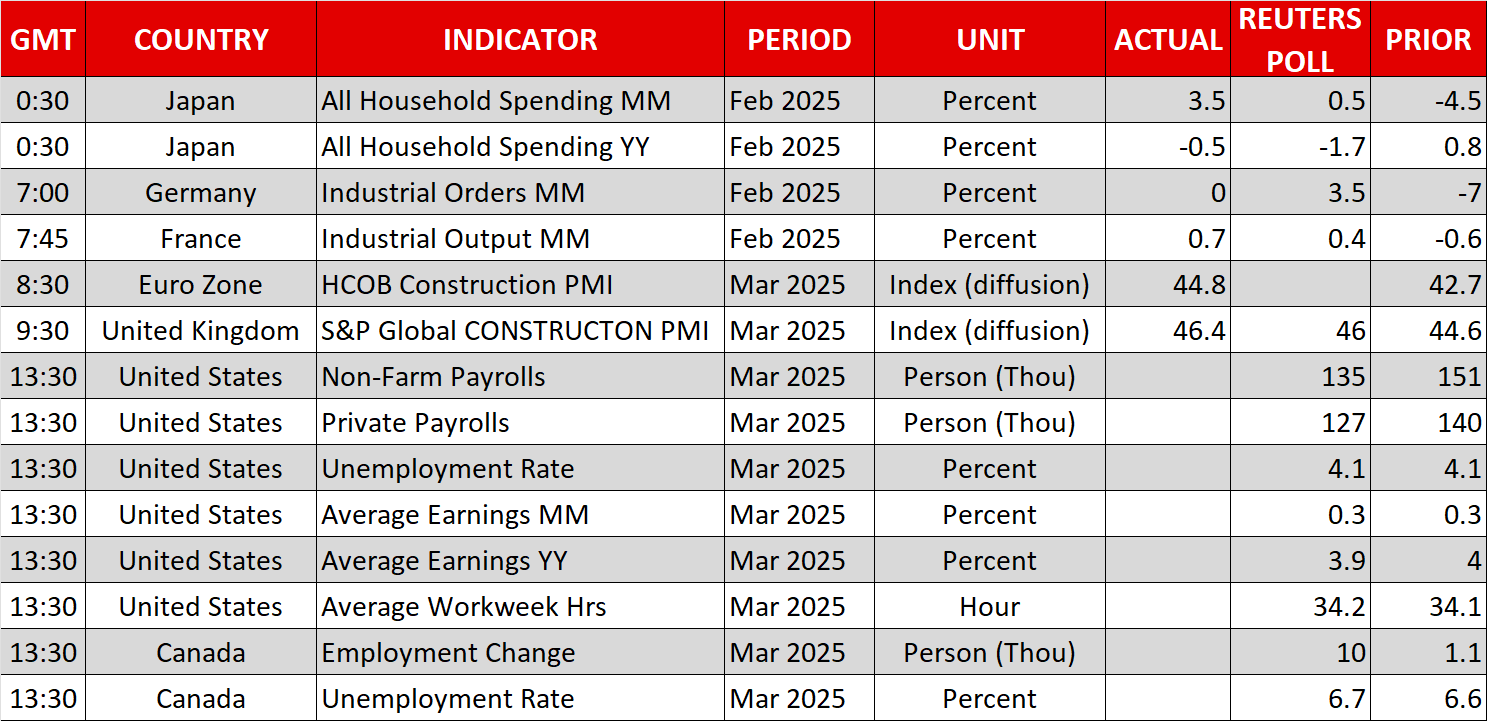

The ADP employment and ISM services readings were somewhat more encouraging than the ISM’s manufacturing PMI from earlier in the week. If the official jobs report, which is due before Powell’s remarks, doesn’t ring any alarm bells either, the Fed chief won’t have any reason to change his tune. Yet, markets will be hoping for some words of reassurance so a late rebound in US equities can’t be ruled out.

Dollar licks its wounds

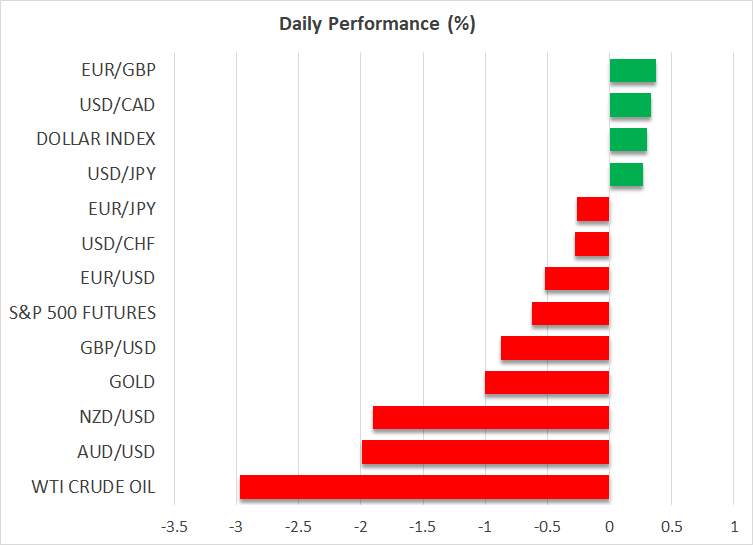

Amidst all the uncertainty, the US dollar has been hammered in FX markets. Its index against a basket of currencies hit a six-month low on Thursday, as the euro briefly spiked above $1.11 and the yen strengthened to 145.18 per dollar.

The greenback appears to be recovering a bit today, as rising rate-cut expectations for other central banks, notably the Bank of England, RBA and RBNZ, are pressuring the other majors.

Moreover, the risk-off sentiment is finally catching up with the risk-sensitive aussie and kiwi. The two are down by almost 2% against the US dollar on Friday.

Gold and oil under pressure as bonds rally

Government bonds have been the surprise beneficiaries of the current risk aversion, with US Treasuries, in particular, rallying hard. This has pushed the 10-year Treasury yield below 4.0% for the first time since October. It’s not clear if recession risks have been fully priced in yet, especially considering how fluid Trump’s tariff policy is, but further declines in bond yields are likely.

Gold, on the other hand, has suffered a setback, sliding below $3,100 to around $3,080. The exclusion of gold and some other metals from reciprocal tariffs is likely behind the pullback, as some investors were stocking up on the precious metal ahead of Trump’s announcement.

Oil futures are the week’s biggest losers, however, as on top of the worsening demand outlook for the commodity, the OPEC and non-OPEC alliance yesterday announced a larger-than-expected increase in production. OPEC+ countries have agreed to pump an extra 411,000 barrels of oil a day starting in May – three times more than the planned amount.

Both WTI and Brent crude futures are extending their decline today, plummeting by around 3.5% to take the weekly losses to between 7% and 8%.

Mad Gold and Oil

The US index's demise has accelerated after confirming the downtrend

Tariff wars made the dollar a risky asset

Market Update: April 4, 2025

USD/JPY collapses to a 6-month low: safe-haven assets in demand

Meet the Challengers Shaping Week 4 of the EBC Million Dollar Trading Challenge II

USDCNH Analysis: Unexpected committee attitude