Yen’s misery worsens, euro lower after CPI dip, dollar awaits Powell

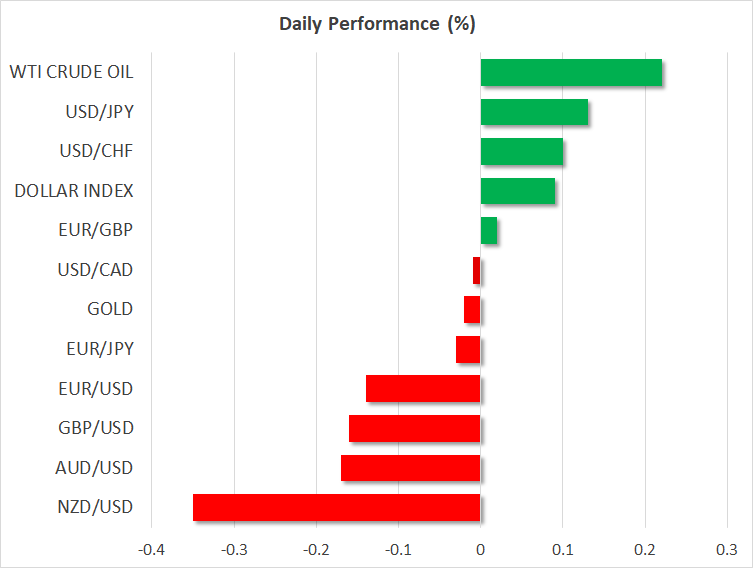

Yen languishes at 38-year low

The Japanese yen ploughed a fresh 38-year low against its US counterpart on Tuesday, hitting 161.75 per dollar, amid ongoing doubts about the Bank of Japan’s ambition to normalize monetary policy and an unexpected pickup in US yields. There’s been no letup in the yen’s slide over the past month, yet there’s been a notable absence of verbal warnings by Japanese officials during this latest phase of depreciation.

Japan’s finance minister, Shunichi Suzuki, provided the usual commentary that the government continues to watch the market closely, but there was no explicit intervention warning. Whilst it’s possible that Suzuki may not want to take any action until the newly appointed vice finance minister for international affairs, who’s in charge of exchange rate policy, takes up his post on July 31, it could also be an indication that the tolerance level for FX intervention has risen.

But in some relief for the yen, the currency was trading slightly firmer against other majors, with the weakness against the dollar mostly down to a stronger greenback.

Dollar extends gains

Although investors have grown more confident lately that the Federal Reserve will be able to slash rates twice this year, the dollar has been in a shallow uptrend since early June, as other central banks are ahead in the race to cut. In recent days, the dollar has been supported by rising Treasury yields, lifted by Donald Trump’s improved prospects of winning November’s presidential election after Biden’s dismal performance in last week’s TV debate.

A Trump presidency is seen as cutting taxes, which would likely add to America’s already very high national debt.

The reluctance of Fed officials to ease up on their hawkish stance has also been keeping the dollar elevated. Friday’s drop in core PCE inflation and yesterday’s weaker-than-expected ISM manufacturing PMI were the latest evidence that inflationary pressures are subsiding and that the economy is cooling somewhat.

Fed Chair Jerome Powell is due to participate in a panel discussion with ECB President Christine Lagarde at the ECB’s annual forum in Sintra, Portugal, at 13:30 GMT. Any suggestion by Powell that a September rate cut could be on the table might see the dollar pull back.

Euro weighed by politics and CPI fall

As for the euro, the primary focus right now is on France’s legislative election, where parties are racing to form alliances ahead of the second vote on Sunday. Even though the National Rally party took the lead in the first round, tactical voting could prevent it from forming a government after the second round. With many constituencies facing a three-way runoff, the centrist and left-wing alliances are encouraging their candidates that came third to stand down to give the second-placed candidate a better chance of beating the National Rally candidate.

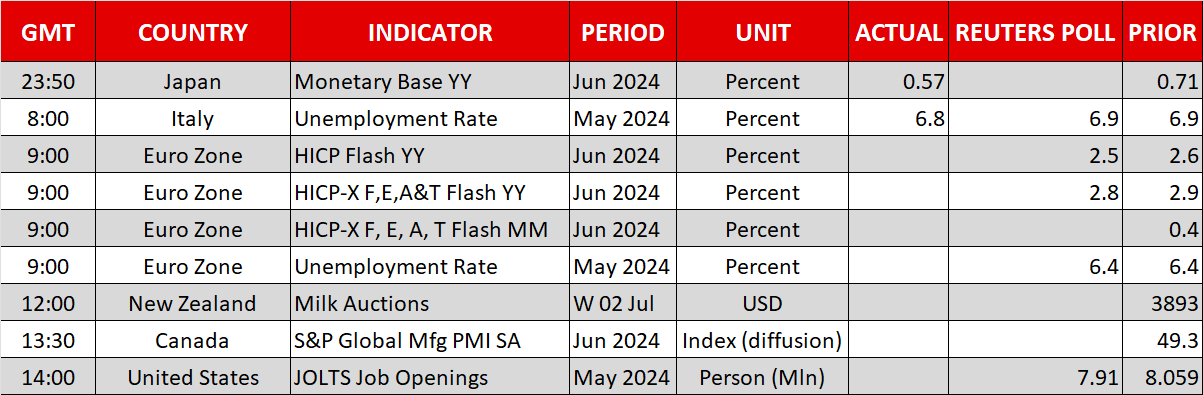

Although this is more likely to lead to a hung parliament, it might be preferable, for investors, to having the far right in power, hence, the euro could gain on the back of it. Today, however, the euro is on the backfoot following the flash CPI readings that showed headline inflation fell back to 2.5% in June, boosting the odds of additional rate cuts this year.

Later in the day, the JOLTS job openings out of the US will be watched ahead of Friday’s jobs report.

Dollar rebounds, loonie tumbles on Trump tariff threats

Crypto market deepens correction

EBC Markets Briefing | Bullion unchanged after Trump tariff vow

NZD/USD Hits Yearly Low Amid US Dollar Strength

Daily Global Market Update

Trump’s Tariff Policies Push Dollar Higher

NZDUSD, USDJPY, EURUSD