US retail sales eyed after CPI report fails to set off fireworks

US CPI does little for 50-bps cut hopes

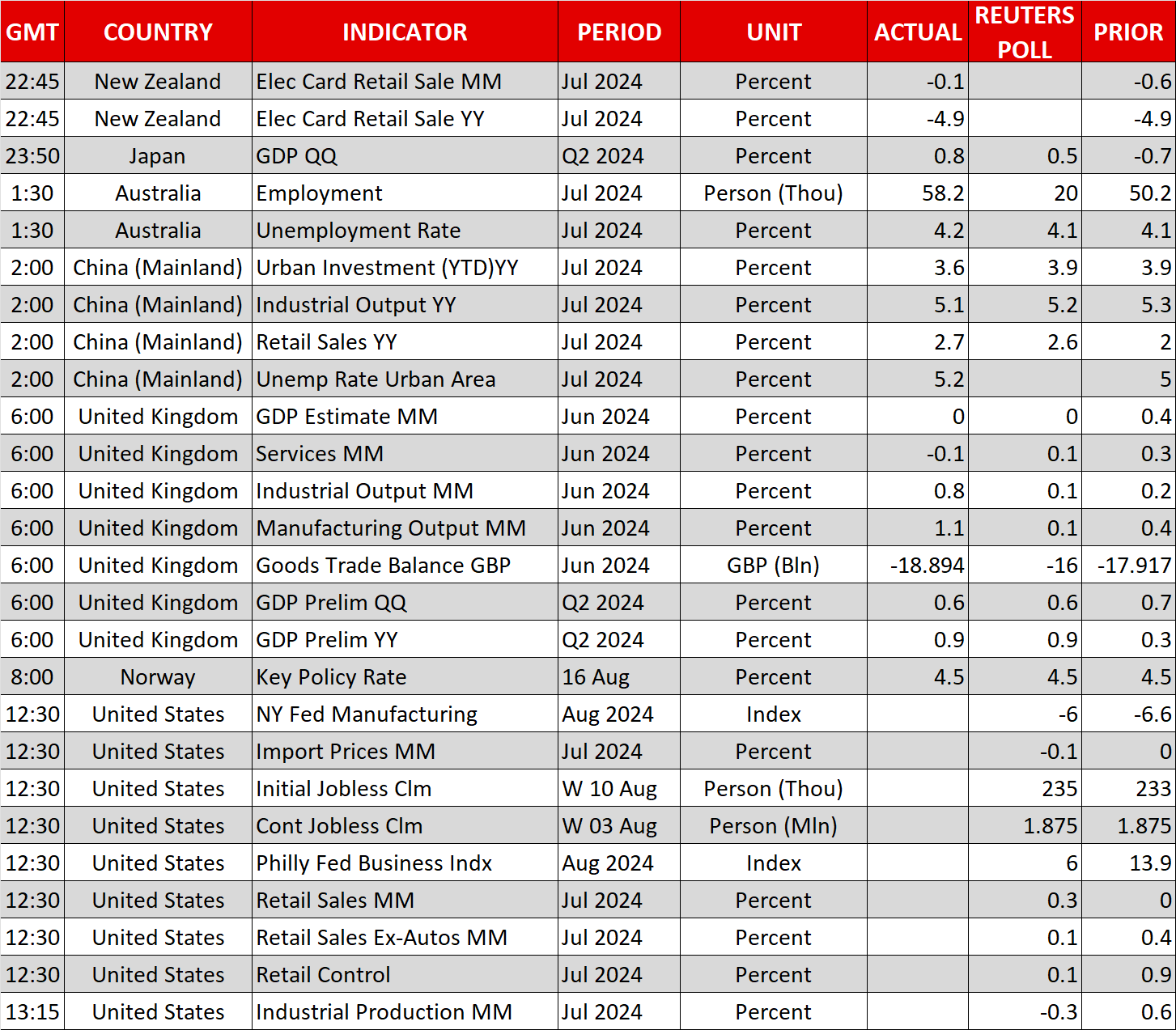

The steady recovery in risk appetite remains on track following yesterday's inflation numbers out of the US that seem to have somewhat underwhelmed investors. Headline CPI eased to 2.9% y/y in July instead of staying unchanged at 3.0% as expected, while core CPI edged down to 3.2% y/y.

Although there were no elements within the CPI breakdown that raised red flags apart perhaps from the continued stickiness in shelter inflation, investors were probably hoping for an even softer report.

With the market panic about a US recession receding following some reassuring data, the CPI readings were the last hope for traders putting money on a major dovish pivot by the Fed next week when policymakers will gather for the central bank’s annual economic symposium in Jackson Hole.

In reality, we are back where we started from before all the scare about a recession sparked turmoil in financial markets. Expectations for a 50-basis-point rate cut in September have gone from being fully priced in at the height of the panic to being less than 40% priced in.

Retail sales could stir things up before Jackson Hole

The ‘disappointment’ in the CPI numbers has turned the spotlight to today’s retail sales figures. Markets are likely to react strongly to either a big downside or upside surprise as the former could revive recession fears while the latter would further dash expectations for aggressive rate cuts.

Weekly jobless claims will also be important, but in the bigger picture, markets are now likely entering a consolidation period that will last until Fed chair Powell's keynote speech at the three-day Jackson Hole Conference that starts on August 22.

Modest gains for Wall Street

On Wall Street, the Dow Jones led the gains as the Nasdaq barely closed in the green on Wednesday, weighed down by a sharp drop in Google parent Alphabet’s shares. The US Justice Department is considering breaking up the Internet giant over concerns about the monopoly power that Google Search has in online ads and searches.

However, e-mini futures point to firmer gains on Thursday for the Nasdaq and global indices are also extending their rebound, aided by fairly upbeat growth data out of the UK, Japan and China.

Yen, pound and aussie cheered by data

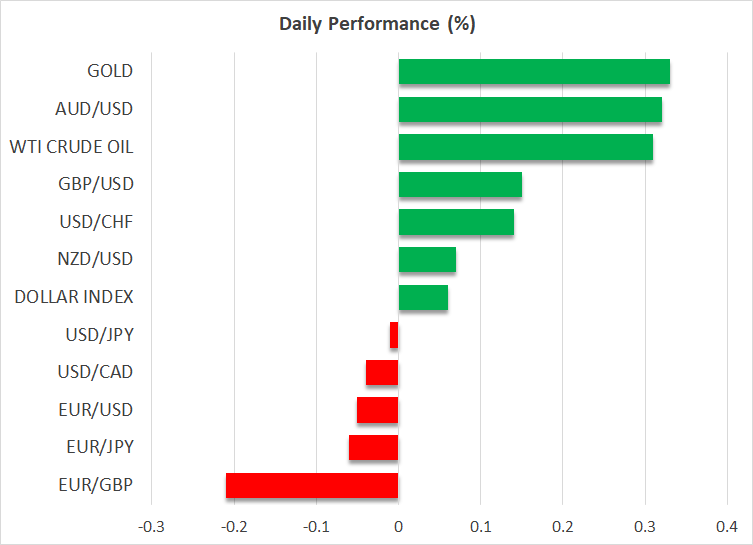

The Japanese economy expanded by a stronger-than-expected 0.8% q/q in Q2, ending three quarters of stagnation and boosting the likelihood of further rate increases by the Bank of Japan this year. The yen inched higher against the US dollar, maintaining the tight sideways range of the past week.

The pound also got a slight lift from solid UK GDP growth of 0.6% q/q, which was in line with forecasts. Although UK inflation is finally under control, the improving growth picture is putting a floor under sterling even as the Bank of England is expected to make further rate cuts this year.

Another currency advancing against the greenback today is the Australian dollar. There’s been some mixed data out of Australia and China today, but the main takeaway is that Australia’s labour market remains resilient, while in China, there are some signs of stabilization in consumer spending.

Yet, the slowdown in investment and a steeper fall in house prices in July has raised hopes that Beijing will announce more stimulus measures soon, and this is supporting the positive sentiment.

Dollar Plummet on Trump’s Treasury Secretary Speculation

Australia's Path to Recovery Economic Outlook for 2025

What’s Next for USD, CAD, and AUD?

EUR, GBP, and JPY Navigate Geopolitical and Economic Crosswinds

Yen Strengthens on BoJ Speculation, Euro Struggles Amid Trade Tensions

Geopolitical Fault Lines: Uneven Ripples Across Global Energy Markets

EBC Markets Briefing | Swiss franc heads for weekly gain in months