Relief rally from soft US CPI falters as trade war escalates

US inflation slows more than expected

There was some relief for markets on Wednesday after US consumer prices moderated more than anticipated in February, reinforcing bets that the Fed will resume its rate-cutting cycle later in the year. The headline rate of CPI fell from 3.0% to 2.8% y/y, below the forecast of 2.9%, while core CPI eased from 3.3% to 3.1% y/y. On a month-on-month basis, the consumer price index rose at the slowest pace since October.

The data is good news for the Fed as it gears up for the March 18-19 policy meeting. Whilst the Fed is almost certain to keep rates unchanged next week, FOMC members are more likely to pencil in additional rate cuts for 2025 in their dot plot now that the inflation picture is finally turning more favorable, particularly as services CPI is also coming down.

Counter-tariffs dent sentiment

Wall Street cheered the soft CPI report, albeit in a subdued fashion. The S&P 500 ended the session 0.5% higher, while the Nasdaq 100 was up 1.1%. But futures have turned negative today, with shares in Europe also in the red.

It proved difficult for investors to maintain the CPI-led optimism for long as the trade war took another turn for the worse. Both Canada and the European Union announced retaliatory tariffs against the United States as the 25% levies on all steel and aluminum imports announced by President Trump in February went into effect yesterday.

Canada said it will impose tariffs of about $20 billion on US goods, while the EU announced $28 billion worth of duties. Trump has promised a response, raising the risk of a further escalation between the major trading partners.

Fed rate cut bets little changed

Any boost to Fed rate cut expectations from the CPI data has been offset by the worsening trade outlook, with investors now pricing in just under three 25-bps-rate cuts for the year amid worries about the inflationary impact of tariffs.

The Trump administration may have blinked a few times in the trade negotiations but it’s yet to cave in to Wall Street traders. Even with the S&P 500 being on the verge of entering correction territory, Trump is refusing to ease up on his trade rhetoric. This is making investors nervous as they continue to fret about what impact the increased protectionism will have on the US and global economy, with the risk of a recession remaining elevated.

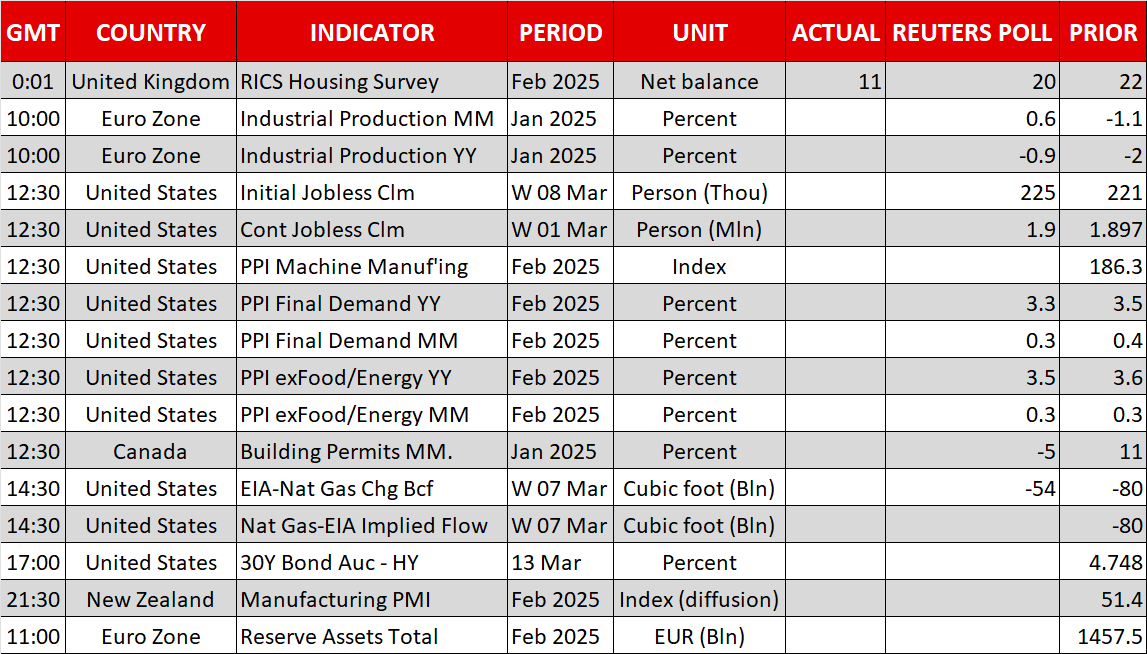

Trading conditions are likely to remain choppy today as the producer price index and the latest weekly jobless claims are due at 12:30 GMT.

Markets will also be watching for any updates from Congress about a possible deal on a stopgap funding bill. The House passed its spending bill on Tuesday, but Senate Democrats have rejected the measures. Republicans will need the support of at least eight Democrats for the legislation to pass the Senate, otherwise, the government could shut down on Saturday.

Dollar off lows, yen gets a lift

The US dollar made a modest recovery on Wednesday but is mixed today. The euro’s rally has lost some momentum following the trade flare-up between Washington and Brussels. The head of Germany’s central bank, Joachim Nagel, has warned the economy could tip back into recession if more tariffs are announced.

The Japanese yen was somewhat firmer, though, on Thursday, after Bank of Japan Governor Kazuo Ueda sounded upbeat about wage growth and consumption, suggesting that further rate hikes are likely over the course of the year.

The Canadian dollar remained supported despite the Bank of Canada’s rate cut yesterday and warning of “a new crisis” from Trump’s trade war.

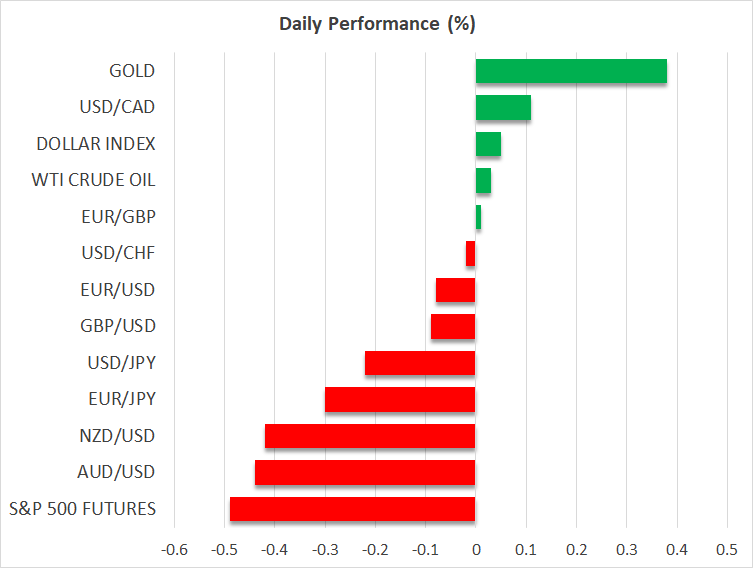

Gold eyes new record

Gold prices edged up for a third day, approaching the $2,950 area where it set a record high on February 24. The growing uncertainty from Trump’s policies is driving investors back to the popular safe haven even as US Treasury yields stage a decent recovery.

There are also doubts as to whether Russia will sign up to the US ceasefire deal that Ukraine has already agreed to. US officials are travelling to Moscow today for talks on a possible deal.

ATFX Market Outlook 14th March 2025

EBC Million Dollar Trading Challenge II | Leaders Fall as Rising Stars Chase 10x Returns

Mood improves as equities rebound but gold and dollar stay bid

Gold poised for record highs strong demand and stable outlook

Daily Global Market Update – 14th March, 2025

EBC Markets Briefing | Chinese stocks are great again

The Truth About Trading Volatility: It’s Not Gambling If You Know This