A way forward: a roundup of recent central bank decisions

By Kyle Rodda, Senior Market Analyst at capital.com

All price information and forecast data in this article is sourced from Reuters and Trading View.

Five of the world’s most significant central banks delivered policy this week. We review the decisions and discuss their impact on the markets.

US Federal Reserve: Sticking to a cutting bias

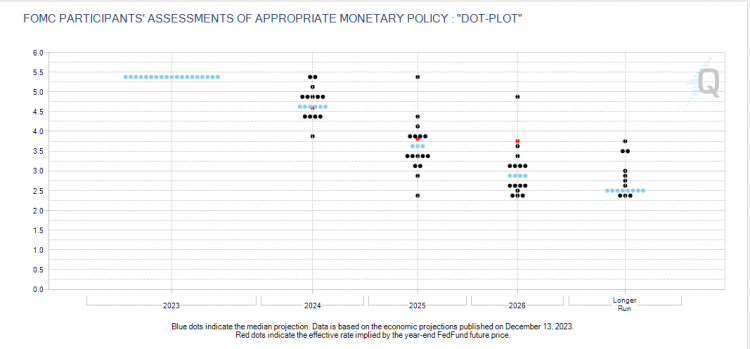

As expected, the US Federal Reserve left policy settings unchanged, including the Federal Funds Rate, which remained at 5.5%. The interest in this FOMC meeting was the Fed’s guidance and whether a recent spate of stronger-than-expected economic data and signs of stickier inflation would lead to a more hawkish policy stance. The Fed maintained its cutting bias while Chairperson Jerome Powell stated in his press conference that the central bank will likely lower interest rates this year.

While the US Federal Reserve remains focused on returning price growth to target, it signalled a willingness to tolerate more persistent inflation to preserve the labour market. The Fed raised its inflation and growth forecasts and lowered its estimates for the unemployment rate but still implied three cuts to the Federal Funds Rate this year. The median projection for rates in 2025 and 2026 was revised upwards to 3.9% and 3.1%, respectively; however, this is lower than the implied path for policy heading into the FOMC meeting.

(Source: CME Group, 20/03/2024)

Financial markets responded bullishly to the FOMC decision. The yield curve bull steepened, indicating lower-than-expected policy rates and a more robust growth and price impulse. The US Dollar subsequently fell. Lower market-implied real rates created better conditions for asset prices. Wall Street hit record highs, led by rate-sensitive sectors, chiefly tech stocks. Gold prices experienced a goldilocks moment, rising towards record highs on a weaker dollar and falling yields.

(Source: Trading View)(Past performance is not a reliable indicator of future results)

Bank of Japan: The first rate hike in 17 years

The Bank of Japan increased its primary policy rate for the first time in seventeen years, lifting rates out of negative territory to a target range of 0.0% to 0.1%. The central bank also tweaked ETF and J-REIT purchases while scrapping its yield curve control policy. The BOJ left its JGB purchases in place in a move that surprised the market.

The decision to tighten policy was signalled by the BOJ well before the meeting, with several leaks to NikkeiAsia in the days before it outlining the plans to raise rates and modify its unconventional policy tools. However, the markets were surprised by the lack of guidance about future policy and any hawkish rhetoric from Governor Kazuo Ueda. As a result, the Yen tumbled and tested new lows across several major G10 currencies, and the Nikkei surged, with the markets lowering expectations for where Japanese rates would eventually peak.

(Source: Trading View)(Past performance is not a reliable indicator of future results)

Bank of England: Policy unchanged but a shift in tone

The Bank of England kept interest rates unchanged at 5.25%. The move was expected, with interest rate markets implying practically no chance of a move at this meeting. The BOE adopted a more dovish tone regarding future policy in part driven by inflation data released the day earlier, which fell more than economists had predicted, as well as recessionary economic conditions. The Monetary Policy Committee vote split also reflected the shift in the consensus view amongst BOE members, with the 8-1 vote at the previous meeting adjusting to 2-6-1.

The markets brought forward expectations of when the first rate cut from the Bank of England will arrive and how many times the central bank will cut in 2024. The odds of a June rate reduction rose above 80%, while the markets have fully baked in three cuts for the year. The shift sparked a drop in the GBP/USD, which added support to a rally in the FTSE100.

(Source: Trading View)(Past performance is not a reliable indicator of future results)

Swiss National Bank: Rates cut as victory against inflation declared

The Swiss National Bank surprised the markets by becoming the first major central bank to lower interest rates. The SNB cut its key rate by 25 basis points to 1.50%, a move that was only ascribed a 37% chance before the decision. The central bank pointed to the fall of inflation in Switzerland back below its 2% target and to 1.2% in February, claiming “the fight against inflation… has been effective”. The decision came despite the SNB forecasting another pick-up in price growth in the Swiss economy this year, with slowing global growth and a relatively stronger Swiss Franc, the central bank followed through with lowering interest rates at this meeting.

Reserve Bank of Australia: Softer language about future policy

The RBA meeting was not considered “live”, with the market’s focus on the central bank’s language regarding future policy. After surprisingly hawkish language at its February meeting, market participants were looking for softer language from the RBA about future rate rises. The central bank rephrased its guidance, shifting from a stance that "a further increase in interest rates cannot be ruled out" to “the Board is not ruling anything in or out”. While subtle and its intent contentious, the markets treated it as a dovish turn by the RBA, with the futures suggesting a higher probability of two rate cuts this year. The dynamic pushed the AUD/USD lower and the ASX 200 higher.

All price information and forecast data in this article is sourced from Reuters and Trading View.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 84.01% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Past performance is no guarantee of future results. Professional clients can lose more than they deposit. All trading involves risk.

The present marketing communication is not intended for UK audiences.

THE PRESENT MATERIAL MUST BE REGARDED AS MARKETING COMMUNICATION AND SHOULD NOT BE INTERPRETED AS INVESTMENT RESEARCH OR INVESTMENT ADVICE.

The content of this communication has been prepared solely for information purposes and should be considered as such. This communication does not constitute research in accordance with the legal requirements designed to promote investment research independence. While the information in this communication, or on which this communication is based, has been obtained from sources that Capital.com believes to be reliable and accurate, it has not undergone independent verification. No representation or warranty, whether expressed or implied, is made as to the accuracy or completeness of any information obtained from third parties.

The information provided as at the date of this communication is subject to change without prior notice. It does not take into consideration the investors’ individual circumstances or objectives and should not be construed as specific advice on the suitability of any investment decision. Investors should consider this report as merely one factor in making any investment decisions. To the extent permitted by law, neither Capital.com nor any of its employees or affiliates accept any liability whatsoever for any direct or consequential loss arising, directly or indirectly, from any use of this communication or its contents. Any person acting on the information does so entirely at their own risk. Any information that may be provided in this communication relating to past performance is not a reliable indicator of future results or performance.

Capital Com SV Investments Limited (“CCSV”) is registered in Cyprus with company registration number HE354252. CCSV is regulated by Cyprus Securities and Exchange Commission (CySEC) under licence number 319/17. Capital Com Online Investments Ltd is a limited liability company (company number 209236B) registered in the Commonwealth of The Bahamas and authorised to carry on Securities Business by the Securities by the Securities Commission of The Bahamas (“SCB”) with licence number SIA-F245.

Source: https://capital.com/a-way-forward-a-roundup-of-recent-central-bank-decisions

Japanese Yen Strong on Heighten Likelihood of BoJ Rate Hike

Daily Global Market Update

Gold Decline on Easing Geopolitical Tension

How Global Economic Shifts Shape November's Trading Opportunities

Daily Global Market Update

All Eye on Today’s PCE

Daily Global Market Update