US dollar on the back foot as nervousness lingers in equity markets

Dollar is on the back foot today

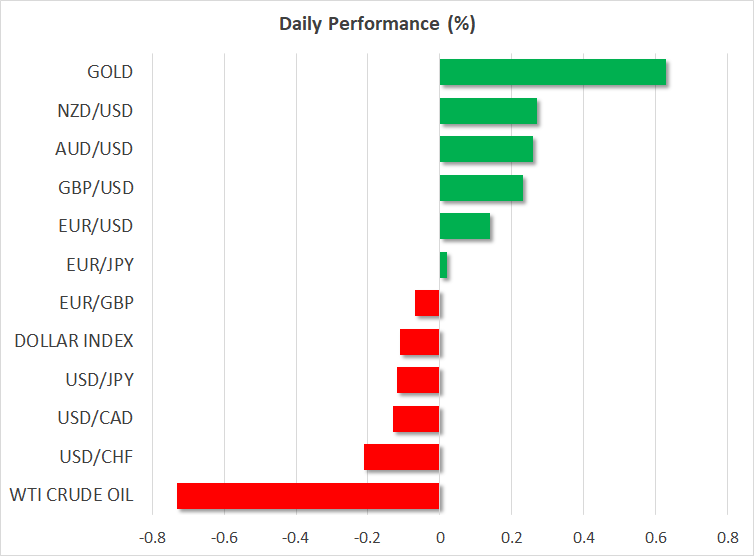

Euro/dollar is rising today after testing the 1.06 level. The combination of dovish commentary from the ECB and hawkish Fedspeak, which played a key role in the recent dollar outperformance, appears to have lost its market-moving ability today as investors are trying to understand the Fed’s thinking.

Following the strong US CPI report, there has been a barrage of hawkish comments pointing to a delay to the first Fed rate cut. The market has taken notice of this rhetoric change and it is currently fully pricing in the first 25bps rate move in November 2024. Yesterday’s Beige Book was less optimistic than some expected but the market is already looking ahead to the next key US data releases. Next week’s durable goods orders and the March PCE report could potentially affect market sentiment and influence Fed members’ stance.

Stock indices appear confused again

US stock indices remain under pressure with the S&P 500 index recording its fourth consecutive red session. Putting aside the performance during the 2023 festive period, one must go back to October 2023 for a similar negative sequence. Back then, weak economic data drove the correction and essentially fueled expectations for a Fed monetary policy easing spree during 2024. Now, strong data releases, which are postponing the Fed rate cuts, and the busy earning calendar are creating nervousness in the market.

Could the June ECB rate cut be postponed?

Developments in the Middle East and the negative reports from the Ukraine front, are casting doubt on the much-touted ECB rate cut. What looked like a done-deal for June could be postponed until July giving the ECB extra time to become more confident about the direction of inflation for the rest of 2024. Seven ECB members were on the wires yesterday and at least four are expected today, who are unlikely to deviate from the script.

Dollar/yen lower again as market prepares for CPI update

The yen is trying to cover some of the lost ground against the dollar, but the pair remains very close to the 34-year high of 154.78. There are daily verbal interventions from Japanese officials, but their effectiveness is questionable at this juncture. Tomorrow, the March inflation report will be published. With the Tokyo CPI released in late March showing mixed results, the market is looking for another small easing in inflationary pressures on a national level.

The BoJ is probably satisfied with both headline and core inflation indicators remaining north of 2%. An upside surprise tomorrow along with the recent rally in oil prices and the ongoing yen weakness keeping the door open to higher imported inflation, could allow the BoJ to appear a tad more hawkish at next week's meeting. The market appears convinced that at least two 10bps rate hikes will be announced this year.

EBC Markets Briefing | Oil prices meander on OPEC’s efforts

Dollar extends retreat ahead of US Thanksgiving

Japanese Yen Climbs to Five-Week High Due to USD Weakness

EURJPY bears stay in control

Daily Global Market Update

Gold Decline on Easing Geopolitical Tension

How Global Economic Shifts Shape November's Trading Opportunities