Dollar starts 2025 on a cautious note

Will king dollar keep its throne?

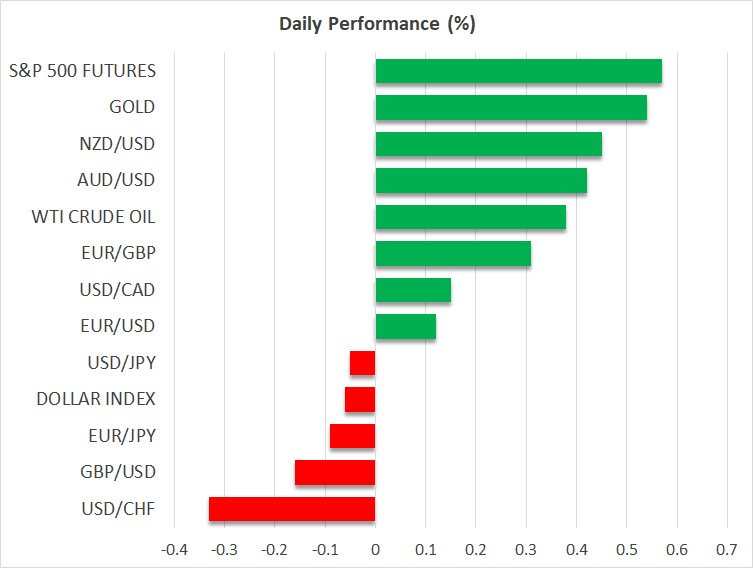

The US dollar traded higher on Tuesday, ending 2024 on the front foot against all its major peers. The greenback entered 2025 on a weaker note, opening today’s session with a small negative gap, but without any important catalyst behind the retreat.

The fundamental landscape for the US currency remains the same. A hawkish Fed, scaling back its rate cut projections to signal only two quarter-point reductions by December, resulted in narrowing yield differentials between the US and other major economies, whose central banks began leaning towards a more dovish stance towards the end of 2024.

One major variable for this development was the election of Donald Trump as the 47th President of the US. Trump has pledged to impose massive tariffs on imported goods from around the globe, especially China, and promised massive corporate tax cuts.

His policies were seen by investors as refueling inflation and thereby lessening the need for aggressive rate cuts by the Fed, while other major central banks appeared concerned about the potential impact of Trump’s policies on their domestic economies.

Stronger than expected US data and sticky inflation, even before Trump’s policies are enacted, were another driver for the greenback. This means that before Trump’s inauguration and any announcement on how he will proceed with his pledges, investors may keep their gaze locked on incoming economic data.

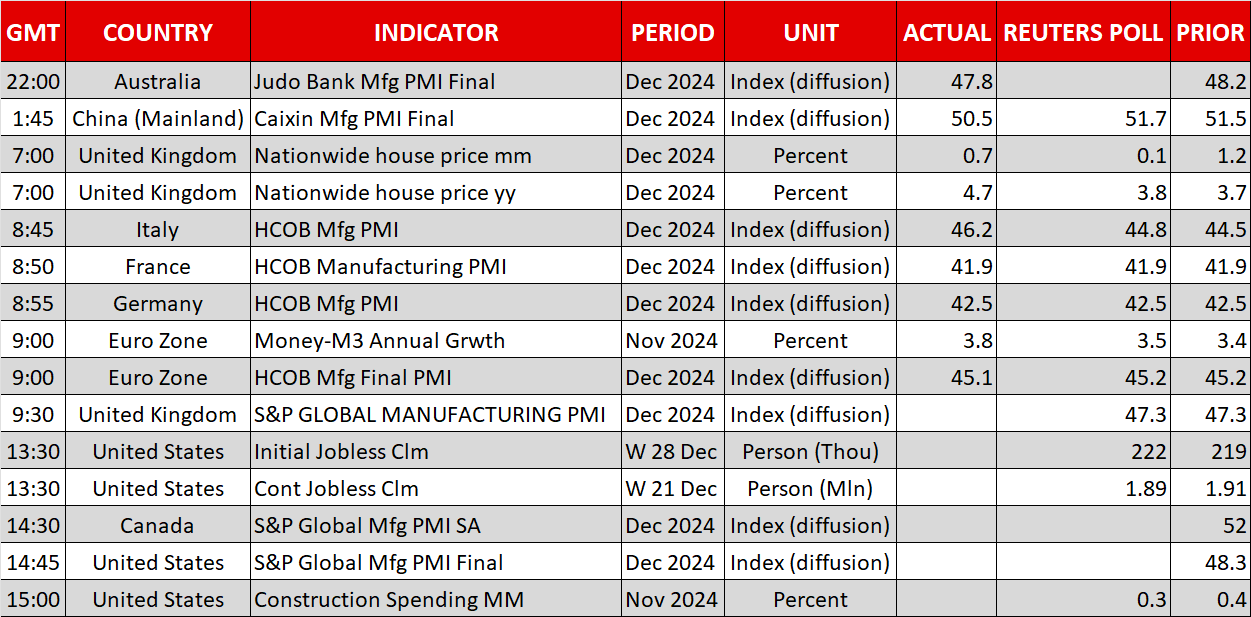

The only noteworthy releases on today’s agenda are the final S&P Global PMIs for December and the initial jobless claims for the last week of 2024. However, next week, the all-important nonfarm payrolls are coming out, where strong job gains and robust earnings growth could corroborate the notion that the Fed does not need to rush into lowering interest rates, thereby allowing the US dollar to continue drifting north.

BoJ dilemma: to hike or not to hike in January?

The only major central bank that has been on a rate-hike cycle is the BoJ, and yet, the yen finished 2024 as the second worst performing major currency, hovering near five-month lows as the BoJ continued to disappoint hawkish market expectations.

At their latest gathering, Japanese policymakers poured cold water on hopes of another rate increase soon, with Governor Ueda highlighting the uncertainty surrounding Trump’s election in the US.

That said, the Summary of Opinions of the December decision revealed that a hike could come sooner than what the market believed after Ueda’s remarks, which combined with the acceleration in the Tokyo CPIs for December prompted market participants to factor in a 50% chance for a quarter-point increase at the upcoming decision on January 24.

This means that another upset by BoJ officials could lead to deeper wounds for the yen, especially against the all-mighty dollar. Nonetheless, a higher dollar/yen may not be the safest trade in town as further advances may at some point trigger intervention by Japanese authorities.

Wall Street pulls back as investors lock yearly profits

All three of Wall Street’s main indices extended their slide on Tuesday, but stock futures are pointing to a positive open today. Overall, Wall Street enjoyed strong gains in 2024, driven by a euphoria surrounding artificial intelligence (AI) and lower interest rates.

The rally petered out in December as expectations of a slower pace of interest rate cuts by the Fed prohibited a so-called “Santa Rally”, prompting investors to lock some year-end profits. However, with the Fed’s rate trajectory remaining to the downside, it is still too early to start arguing about a major bearish reversal.

Even if rate cuts are served delayed, lower interest rates combined with projections of accelerating earnings growth may keep present values elevated and perhaps allow investors to take advantage of a deeper correction and buy at more attractive levels.

EBC Markets Briefing | Gas prices steady on EU-Russia decoupling

Has USDCAD reached a peak point?

Market uncertainty lingers

Dollar Strong on Resilient Job Data

Daily Global Market Update

EBC Markets Briefing | Rand weakness resumes to begin 2025

Gold prices hit the best annual performance since 2010 Let‘s focus on US employment data for the day