Auto tariff relief keeps risk appetite alive; loonie wobbles on Carney win

Trump to relax tariffs on auto industries

The Trump administration has given its strongest indication yet that some tariff reprieve is on the way for America’s car manufacturers, which have been heavily burdened by the steep levies imposed on the whole industry. US Commerce Secretary Howard Lutnick issued a statement on Monday suggesting that a deal had been struck between the White House and domestic car producers, confirming an earlier report by the Wall Street Journal.

The details will likely be unveiled later on Tuesday by President Trump, who is symbolically travelling to Michigan – America’s automotive heartland – to mark his first 100 days in office. Trump will most probably exempt some imported auto parts from the tariffs as well as exclude autos from the separate duties on steel and aluminium.

Muted reaction amid ongoing trade uncertainty

US stock futures were modestly higher at the start of European trading on Tuesday, as investors reserved their excitement until the actual announcement, with some caution ahead of this week’s US economic gauges also holding back gains. But another explanation is the apparent lack of progress in Sino-US trade talks.

Treasury Secretary Scott Bessent told CNBC on Monday that the ball is in China’s court and that the US is focusing on trade negotiations with 15-17 other countries deemed to be more of a priority, hinting that a deal with India is imminent.

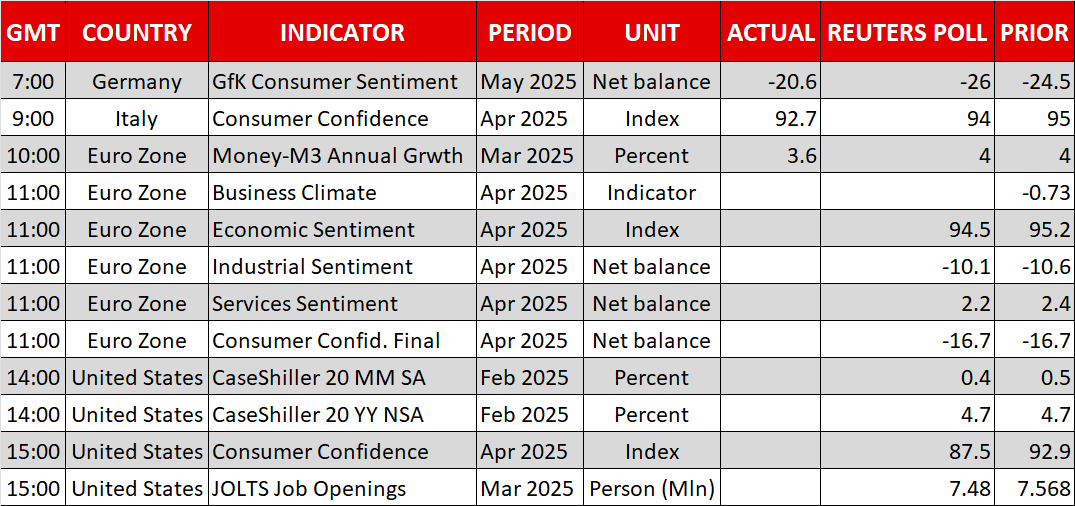

European indices are following Wall Street higher today, as equity markets extend their rebound from the ‘Liberation Day’ selloff. However, despite a five-day winning streak, the S&P 500’s recovery could be losing steam and much will depend on the upcoming Big Tech earnings as well as US data.

Visa, Coca-Cola, Pfizer and BP are some of today’s earnings highlights, while on the data front, the consumer confidence index for April and JOLTS job openings will kick things off ahead of tomorrow’s crucial advance GDP and PCE inflation readings.

Dollar inches up, awaits cues

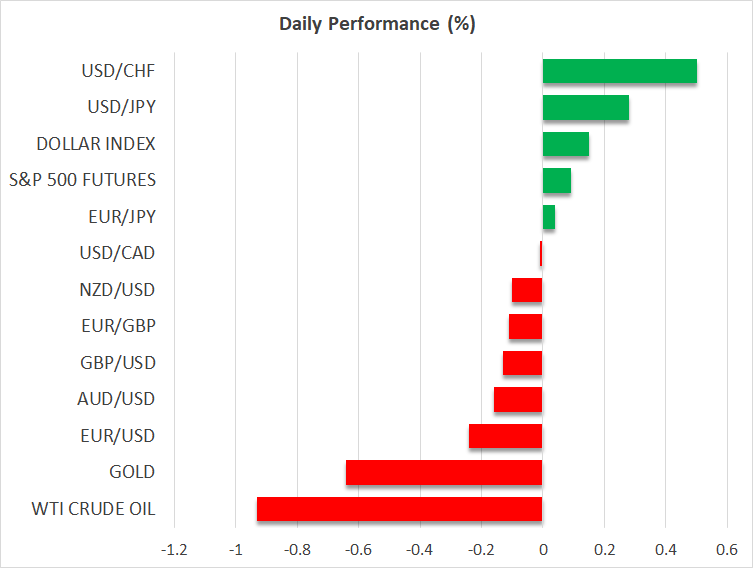

In the currency markets, the major pairs maintained their recent consolidation ranges. Whilst intra-day trading remains choppy, there seems to be a reluctance to push the US dollar significantly higher or lower as investors seek more clarity on Trump’s tariff policy.

There have been some exceptions, however, as both the pound and Australian dollar managed to brush fresh highs in the last 24-hours, reaching three-year and four-month peaks, respectively.

Still, the greenback is slightly firmer today against a basket of currencies, climbing the most against its safe-haven counterparts, the Japanese yen and Swiss franc.

Loonie unimpressed by election outcome, gold slides

The Canadian dollar, on the other hand, see-sawed against the US currency as Canada’s election results came in, but stayed within a tight range. The loonie spiked to C$1.3806/dollar, as Liberal leader Mark Carney looked set to become Canada’s next prime minister. But it fell to C$1.3871/dollar when it became clear that his party is unlikely to gain enough seats for an overall majority, meaning that he will have to form a minority government.

A minority government is probably not the best outcome for Carney, who was hoping to be elected on a much stronger mandate to take on President Trump in what is a pivotal moment for the country, amid the tariff war and intense White House pressure to become America’s 51st state.

On the whole, though, the market mood is still one of ‘wait-and-see’ and even gold is directionless. The precious metal continues to consolidate its recent record run, which came to a halt last Tuesday. It was last trading about 0.8% lower around $3,314/oz.

GBP/USD Hits New High: The Pound Defies Market Pressures

USDJPY Analysis: Clear Direction Ahead

5 Traders Who Stood Out in Week 8 of EBC’s Million Dollar Trading Challenge II

ATFX Market Outlook 29th April 2025

Technical Outlook on USDJPY, EURUSD, BTCUSD

Dollar’s struggles continue as tariffs remain in focus

Gold Under Pressure as Market Hopes for US-China Trade Progress