Yen tumbles to fresh lows, dollar awaits GDP

Will Ueda appear in a hawkish suit this time?

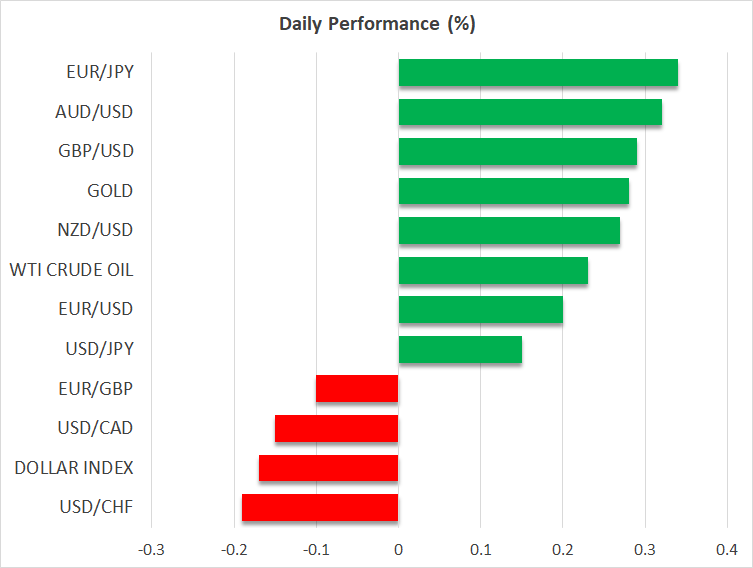

The yen extended its tumble to a fresh 34-year low, falling below 155.00 per dollar. With less than 24 hours to go for the Bank of Japan’s decision, investors are likely sitting on the edge of their seats in anticipation of the gathering’s outcome.

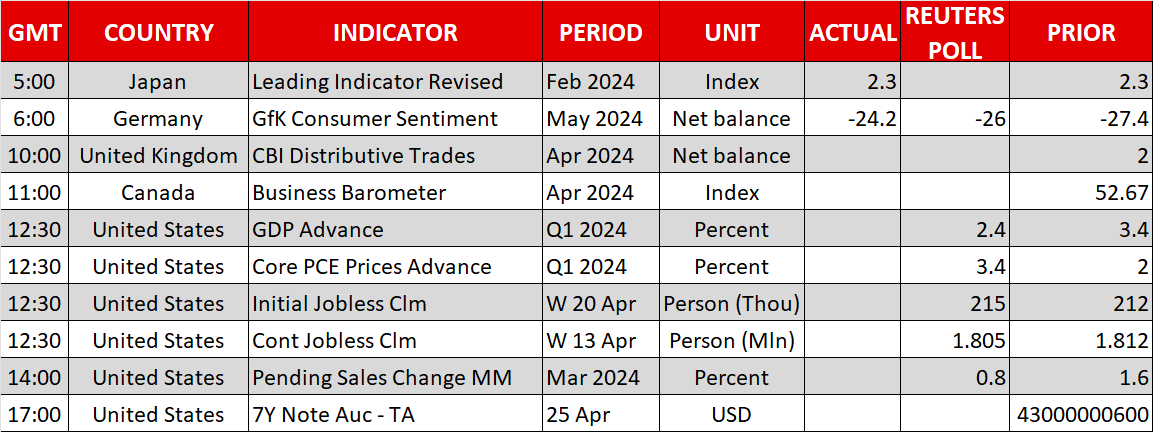

Recently, Governor Ueda said that they may raise interest rates if the yen’s declines result in accelerating inflation and added that they could begin reducing their huge bond buying at some point. With inflation accelerating notably in February, despite ticking a bit down in March, and taking into account that the wage negotiations resulted in the largest pay hikes in 33 years, investors may be on the lookout for hints and clues on how soon the next hike will be delivered. Currently, they are expecting the next 10bps hike in June.

However, the BoJ has a history of disappointing hawkish expectations, and thus should this be the case again, the yen is likely to continue falling and perhaps revive intervention concerns. That said, officials could wait for a while longer before stepping in, given that they have repeatedly warned that they will respond if the moves are speculative and not based on fundamentals. Indeed, they have been silent lately perhaps as the latest leg south in the yen was driven by fundamentals.

On the other hand, Ueda may want to make sure he avoids a 2022 déjà vu, when Kuroda’s dovish remarks pushed the yen off the cliff and forced authorities to intervene and save the currency. So, he could decide to adopt a more hawkish stance.

Will the Fed refrain from cutting rates this year?

Although it gained ground against the yen, the dollar traded on the back foot against most of its major peers, perhaps as traders were reluctant to initiate new long positions ahead of the US GDP data later today.

Expectations suggest that growth in the world’s largest economy slowed to an annualized 2.4 q/q in Q1 from 3.4%, but with the Atlanta Fed GDPNow model pointing to a 2.7% growth rate, the risks may be titled to the upside. Following the downside in the S&P Global PMIs on Monday, investors may need to see stellar GDP data before they further scale back their rate cut bets, and thereby allow the dollar to stage a comeback.

Wall Street set to open lower, gold extends correction

US equities closed mixed on Wednesday as stock traders remained cautious as well ahead of the GDP data. However, after the closing bell, although Meta reported better than expected results for Q1, its shares plunged more than 15% on weak revenue guidance, increasing the risks for a lower open on Wall Street today. The tech earnings continue today with results from Microsoft and Alphabet.

Gold traded a bit lower yesterday as the easing geopolitical tensions allowed investors to continue offloading safe-haven positions. However, central bank buying, and strong Chinese demand remain big supportive factors, keeping the outlook positive. What's more, although delayed, the next move on US interest rates is more likely to be a cut, which is positive for the yellow metal.

EBC Markets Briefing | Oil prices meander on OPEC’s efforts

Dollar extends retreat ahead of US Thanksgiving

Japanese Yen Climbs to Five-Week High Due to USD Weakness

EURJPY bears stay in control

Daily Global Market Update

Gold Decline on Easing Geopolitical Tension

How Global Economic Shifts Shape November's Trading Opportunities