Markets perk up as soft PPI sets the tone ahead of US CPI

Mood brightens ahead of US CPI data

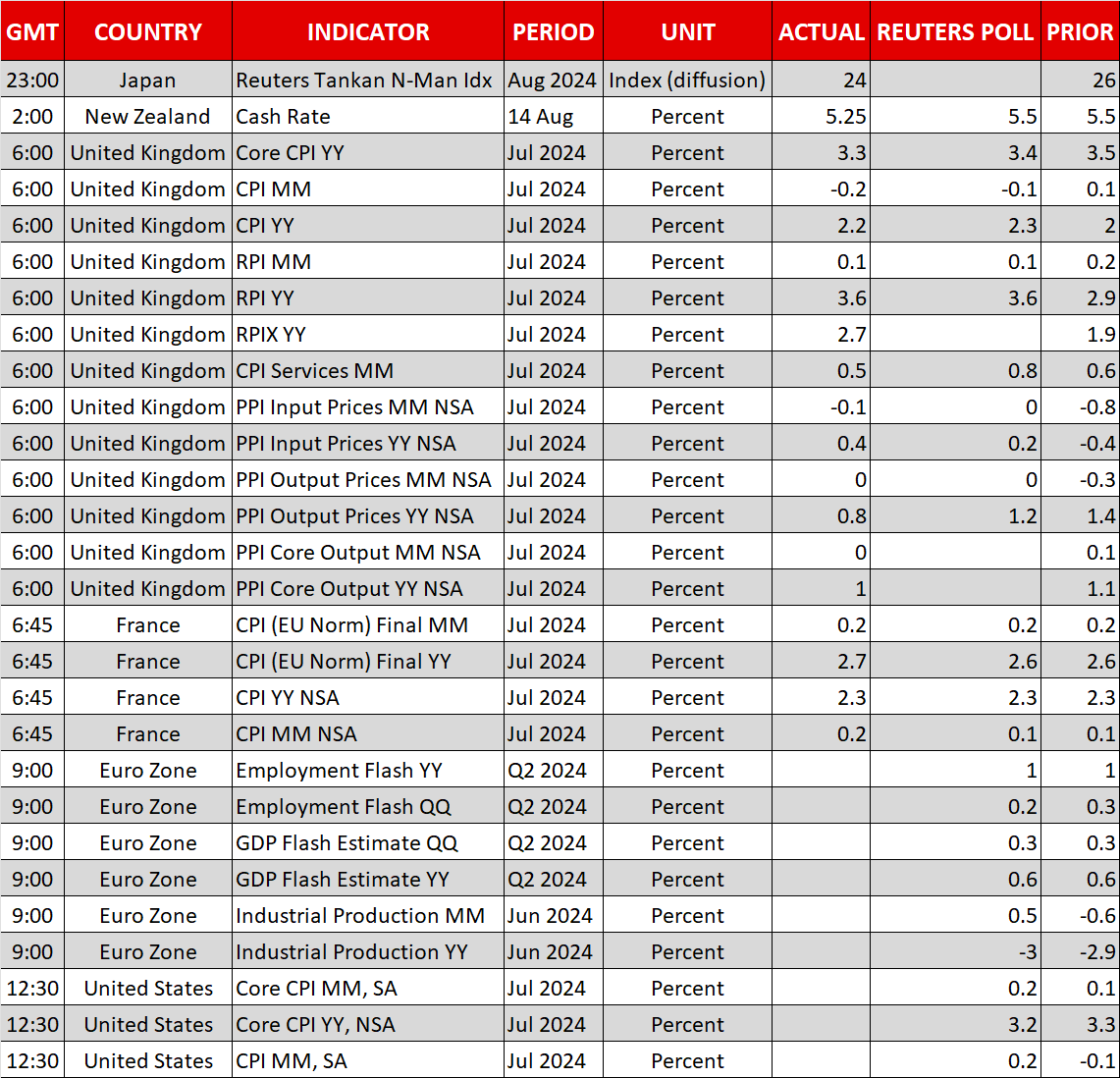

The rebound in equity markets gained further traction on Tuesday after US producer prices rose less than expected in July, raising hopes that today’s report on consumer prices will also surprise to the downside.

Headline inflation in the United States is expected to have stayed unchanged at 3.0% y/y in July, but core CPI is forecast to have edged lower to 3.2% y/y.

The PPI data added fresh fuel to the recovery on Wall Street, with the S&P 500 closing up 1.7% and the Nasdaq 100 by 2.5%. The US dollar tumbled sharply, however, even though the move in Treasury yields was much more modest.

With recession risks ebbing again, an in-line CPI report is unlikely to dent the upbeat mood, but hotter-than-expected readings could deal a blow to the bounce back on Wall Street. Still, a full-blown panic is unlikely in such a scenario as investors might prefer to stay on the sidelines as they wait for Powell’s keynote speech at the Fed’s annual Jackson Hole Symposium next week.

Kiwi dives on ‘surprise’ RBNZ cut

Adding to the sense of optimism is the growing chorus of central banks joining the rate-cut club. The Reserve Bank of New Zealand became the latest to start its easing cycle, announcing a 25-basis-point reduction earlier today. Although the decision was not a complete surprise to traders, economists had anticipated the RBNZ to stay on hold at its August meeting.

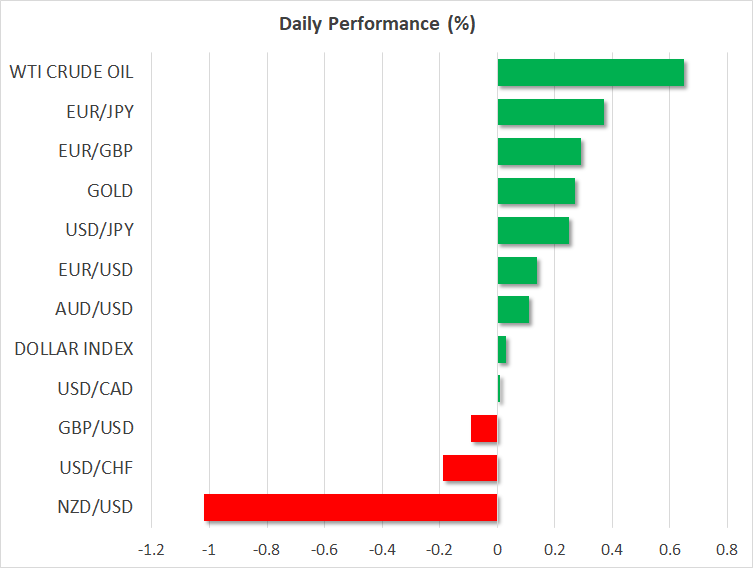

Nevertheless, the New Zealand dollar slid by 1% against its US counterpart on the news as policymakers flagged at least one more cut by year-end. And although the scale of the drop was likely exaggerated by yesterday’s pullback in the greenback, the RBNZ’s complete dovish turn is likely to keep the kiwi on the backfoot in the near term.

UK CPI miss halts pound’s rebound

The UK’s run of pleasing CPI prints continued this month, as inflation data released today showed the headline figure came in slightly below forecasts at 2.2% y/y in July versus the 2.3% expected. More importantly, services CPI eased to 5.2% y/y from 5.7% and it follows yesterday’s similarly encouraging decline in wage growth, both of which have been a thorn in the side of the Bank of England’s fight against inflation.

Subsequently, investors are pricing in a more than 55% probability that the BoE will cut rates again in September and this may prevent the pound from fully retracing the past month’s slide.

Elsewhere, the yen was broadly weaker on the back of the risk-on sentiment, showing little reaction to the Japanese Prime Minister Fumio Kishida’s announcement that he will step down next month.

Gold and oil up on heightened Iran fears

In commodities, gold inched higher from Tuesday’s lows when it fell after failing to break tough resistance in the $2,475/oz area. But with the dollar likely to stay soft and growing fears of an imminent attack by Iran on Israel, the precious metal may yet scale a new all-time high in the coming sessions.

Oil futures were also positive on Wednesday, having slipped yesterday on demand worries. But the elevated risk of an escalation in Middle East tensions is keeping oil supported today.

Australia's Path to Recovery Economic Outlook for 2025

What’s Next for USD, CAD, and AUD?

EUR, GBP, and JPY Navigate Geopolitical and Economic Crosswinds

Yen Strengthens on BoJ Speculation, Euro Struggles Amid Trade Tensions

Geopolitical Fault Lines: Uneven Ripples Across Global Energy Markets

EBC Markets Briefing | Swiss franc heads for weekly gain in months

Dollar and gold gain as geopolitical risks and eurozone data worsen