Dollar and stocks sink as Trump unleashes ‘Liberation Day’

Trump goes for maximalist tariffs approach

US President Donald Trump celebrated his self-proclaimed ‘Liberation Day’ in the White House’s Rose Garden on Wednesday, as he unveiled the full list of countries to be hit with a fresh wave of tariffs. The anxiously awaited reciprocal tariffs met the worst expectations, as no country was spared in Trump’s latest trade tirade.

Trump announced a flat universal tariff rate of 10% on all countries, but 60 countries will be charged with higher duties. Mexico and Canada are exempt from reciprocal tariffs as Trump has already slapped 25% levies on most imports from its bordering neighbours.

Products that fall under the sectoral tariffs such as those on steel and aluminium, and autos, will also not be charged twice. However, there won’t be any such exemptions for China, which has already been imposed 20% tariffs by Trump. Its goods entering the United States will now be levied an additional 34%, taking the total tariffs on China to 54%.

Stocks sink as hopes of compromise dashed

Shares of companies that have a large manufacturing base in the impacted countries such as Apple and Nike plummeted in after-hours trading, while stock markets in Asia and Europe are in a sea of red today.

E-mini futures for the S&P 500 and Nasdaq have slumped by more than 3.0%, though Dow Jones futures are down by a somewhat more moderate 2.5%.

The losses come after a positive close on Wednesday before Trump’s unveiling when there was still some optimism that the reciprocal tariffs might be more measured.

However, with the universal 10% rate due to go into effect on April 5 and the higher rates on April 9, there is very little time for negotiation. Even if at some point over the coming months some of the tariffs are scaled back or fully reversed, the immediate impact of the spike in tariffs on the US economy in the next few days is unavoidable.

US dollar hit by recession risks ahead of NFP

Worries about the economic consequences of Trump’s decisions were also reflected in the US dollar, as the currency slid on recession fears. Investors upped their bets of Fed rate cuts to 80 basis points, fully pricing in three 25-bps reductions for the year.

That seems overly optimistic considering the potential inflationary impact of the latest tariffs. Even if this is the last of the big tariff decisions and it looks very likely that any price increases passed on to the consumer will be transitory, the Fed will probably hold off cutting rates unless there’s a sudden deterioration in the labour market.

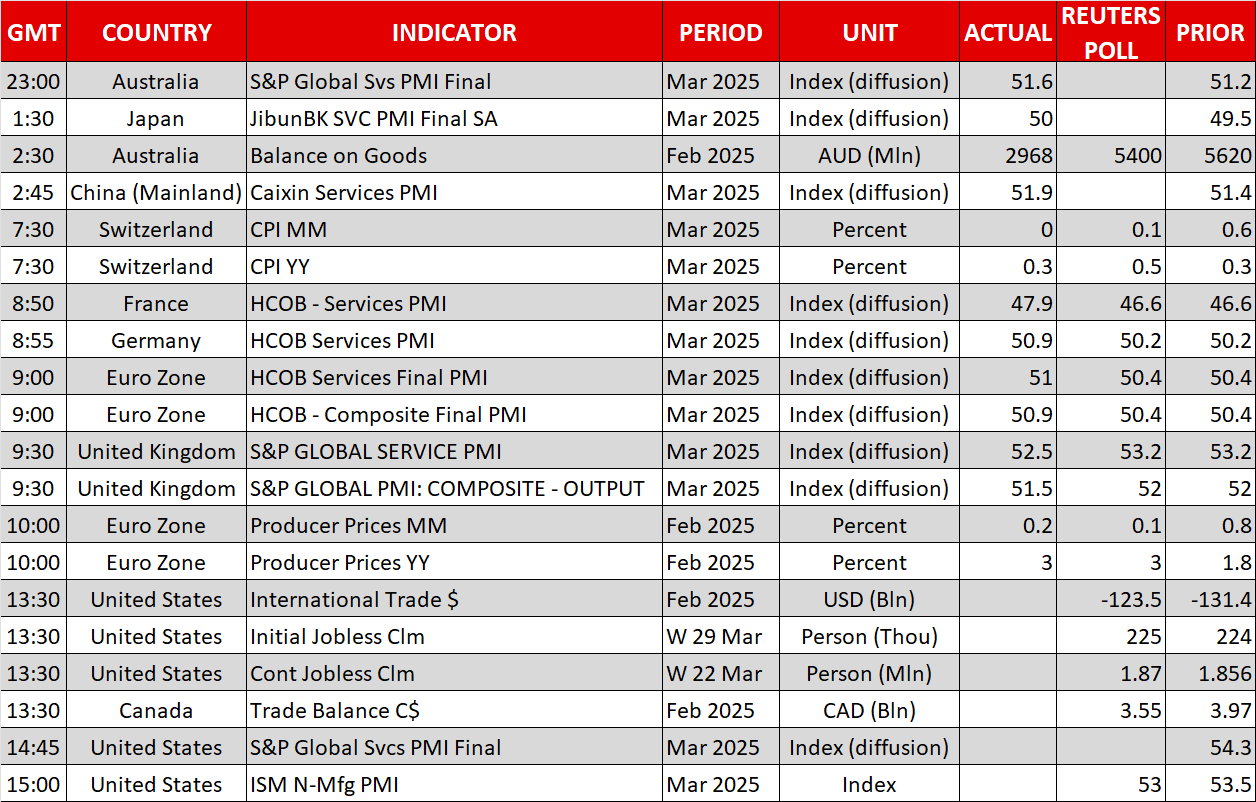

Friday’s nonfarm payrolls report will provide vital clues as to where things stand before the tariffs kick in, as this week’s data out of the US have been mixed. Yesterday’s ADP employment print, which beat expectations, contradicted the gloomier picture from the ISM manufacturing PMI. The ISM services PMI due later today should shed more light, however.

Euro and pound jump, aussie and kiwi can’t keep up

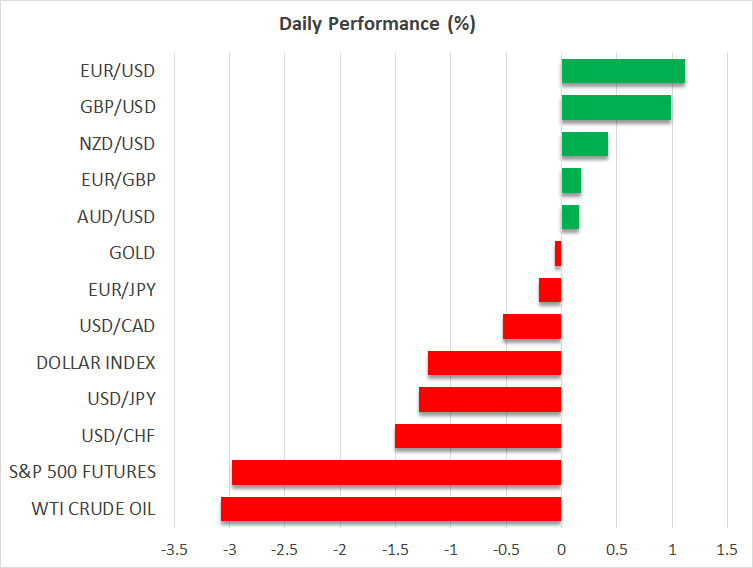

The euro is up more than 1% today, testing the $1.10 level. When comparing the EU’s 20% tariff rate to those of Vietnam and China, it could have been a lot worse for European exporters. The UK got off even more lightly as its exports fall under the 10% flat rate and sterling has surged past the $1.31 level.

The Trump administration’s method of calculating the reciprocal tariffs, which is based on the size of America’s trade deficit with each country, has created winners and losers.

Yet, the safe-have yen and swissie are up the most, ignoring the respective higher duties on Japan and Switzerland, while the antipodean dollars, are only modestly stronger today, despite both Australia and New Zealand falling under the flat rate.

Gold rally runs out of juice, oil slips

Concerns about a global recession are likely weighing on risk-sensitive currencies, including cryptos. Trump’s radical take on trade policy threatens to upend global supply chains and reverse globalization.

All this should be pumping more fuel into gold’s rally, but the precious metal is currently inching lower after hitting a new record peak of $3,167.57/oz earlier today. Gold was looking overbought heading into Trump’s ‘Liberation Day’ so the bulls have likely paused for some breath.

Oil futures, meanwhile, have tumbled by more than 3% amid worries about weaker global demand from Trump’s trade war, as well as on the expectation that OPEC+ will raise production quotas for May when the group concludes its monthly meeting that starts today.

Mad Gold and Oil

The US index's demise has accelerated after confirming the downtrend

Tariff wars made the dollar a risky asset

Market Update: April 4, 2025

Tariff turmoil sends dollar and Wall Street spinning

USD/JPY collapses to a 6-month low: safe-haven assets in demand

Meet the Challengers Shaping Week 4 of the EBC Million Dollar Trading Challenge II